Semi-workshop ini adalah yang pertama di Indonesia, oleh kedua orang instruktur yang pakar dan dua orang pembicara lain yang adalah ketua Himpunan Penerjemah Indonesia dan Ketua Lembaga Sertifikasi Profesi Universitas Indonesia (LSPUI).

Cocok untuk para mahasiswi/-a, penerjemah, juru bahasa, lawyer, notaris, manajer dan sekretaris perusahaan, manajer hukum dan hubungan internasional dll.

Link pendaftaran:

Catatlah waktu dan tanggal penting ini: jam 14.00-17.00 WIB, hari Minggu, 20 November 2022

Untuk informasi lebih lenajut, CV ringkas para pembicara dan instruktur, 10 tanya-jawab yang sering diajukan (FAQs) tentang semi-workshop ini, formulir pendafataran dan petunjuk pengsiannya, silakan kunjungi: www.tjansietek.com

Famous for its five fragrances and varied health benefits

Famous worldwide for its five fragrances and various health benefits, Indonesian white cardamom grows around the country. We export it and many other kinds of organic agricultural product from the country.

For product specifications or more info, please send your inquiries to:

PT Berkah Dewata Agri

228 Prof. Dr. Satrio Road, Jakarta 12940, Indonesia

Mobile & WA numbers: +62822 1000 8628 or +62821 2541 5678

We are an exporter of fine and extra-fine granulated, halal & kosher-certified grade food-grade desiccated coconuts from Indonesia, Southeast Asia, to Europe, Asia etc..

Our products fulfill the requirements of all the importing countries:Codex General Principles of Food Hygiene, EU & FDA Good Manufacturing Practices and comply with all other current national and international food laws and regulations.

SPECIFICCHEMICALPROPERTIES

Moisture Content, % 2.5 maximum

Total Low Fat (dry basis), %: 40%-50% & 45%-55%

Free Fatty Acid (as lauric) dry basis, %: 0.10 maximum

The products can be an important part of the ingredients of your ice cream, cookies, bakery, chocolate, etc., etc. For product specifications or more info, please send your inquiries to:

PT Berkah Dewata Agri

228 Prof. Dr. Satrio Road, Jakarta 12940, Indonesia

Mobile & WA numbers: +62822 1000 8628 or +62821 2541 5678

email: dewata.agri@gmail.com, or tst228@gmail.com

Extra Fine Granules of 40%-50% Low Fat in a 25kg Bag

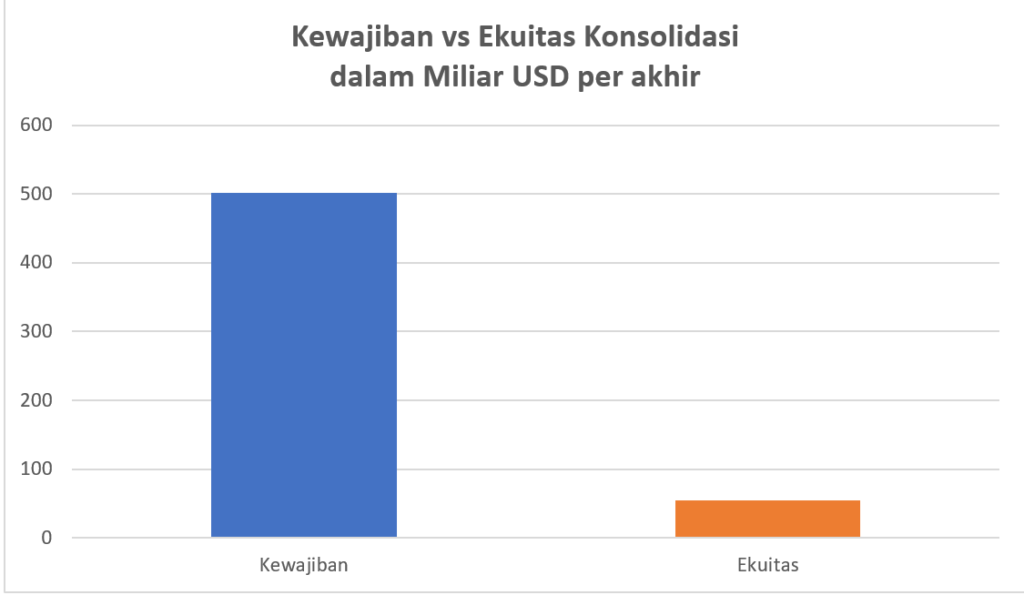

Utang LN Evergrande cuma USD 20 miliar, atau 6,6% dari total kewajiban konsolidasinya yang USD 302 miliar

Utang USD 20 miliar itu dipegang oleh puluhan bank internasional yang asetnya triliunan USD sehingga tidak akan ada masalah sistemik

Selebihnya adalah kepada lembaga keuangan, investor, kontraktor, supplier dll di dalam negeri dan mata uang yuan (CNY; RMB)

Aset fisiknya bernilai USD 220 miliar dan belum revaluasi

Masalah terbesar adalah kewajiban jangka pendeknya (di bawah satu tahun): USD 233,6 miliar & penyelesaian pembangunan sekitar 1,5 juta apartemen yang telah dipesan, yang sebagian telah diberi uang muka dan sebagian lainnya bahkan sudah lunas

Harus jual aset & lakukan restrukturisasi yang luas untuk kewajiban jangka pendek itu untuk meyakinkan para investor, pemberi uang muka, kontraktor dll

Ukuran kewajiban konsolidasi Evergrande kecil sekali terhadap aset total maupun permodalan perbankan China

Jumlah aset konsolidasi grup Evergrande per akhir 2020 adalah USD 356,7 miliar (IDR 5,17 kuadriliun) atau hanya 0,67%, atau 67/10.000 dari jumlah aset perbankan China yang USD 52 triliun (IDR 754 kuadriliun) per akhir Juni 2021 (https://lijusu.com/2021/09/12/terbesar-di-dunia-modal-inti-laba-aset-perbankan-china/). Kewajibannya berjumlah USD 302 miliar dengan catatan kewajiban itu terdiri atas (i) Utang USD 66,6 miliar kepada perbankan, pemegang obligasi dan surat utang lainnya di dalam dan LN; the Financial Times memperkirakan obligasi yang dipegang oleh banyak investor LN berjumlah USD 20 miliar (https://www.ft.com/content/7ac2d661-5a63-4768-91a1-182f02b2afa5); (ii) Pajak USD 32 miliar; dan (iii) Kewajiban pembayaran lain-lain USD 203,4 miliar kepada para kontraktor, pemberi uang muka, supplier, pembeli produk-produk pengelolaan aset dll.

Sumber: laporan Tahun 2020 Evergrande

2. Banyak sekali Aset Fisik Evergrande yang bernilaiTinggi di China

Tanah matang dan mentah itu belum dinilai ulang karena mayoritasnya sudah lama dimiliki oleh Evergrande. Sebagaimana kebiasaan para developer di China, Evergrande membeli tanah mentah secara cash (dengan uang muka dari calon pembeli dan pinjaman lewat obligasi dan surat berharga lainnya yang berjangka pendek & berbunga tinggi) dan biasanya lewat lelang terbuka. Harga tanah dan perumahan/apartemen di China selalu naik setiap tahun, antara 5%-9%.

3. Beda antara Masalah Evergrande dan Lehman Brothers di AS

Lehman Brothers adalah bank investasi, mencari dana dengan menjual reksa dana pasar uang yang berjangka pendek (di bawah satu tahun) dan membeli kewajiban berupa utang yang dijaminkan (CDO; sejenis kontrak sekuritas derivatif) dan obligasi kelas sampah (junk bond). Aset dasar CDO-CDO itu adalah akta gadai perumahan (hipotek), dengan nilai total nominal sekitar USD 650 miliar yang dikreditkan kepada para pembeli yang tidak layak diberi kredit (sub-prime) dengan suku bunga yang tinggi.

Beda nyata dengan Aset Fisik Evergrande: 80% pembeli produk properti Evergrande bonafid (prime) karena mereka memberi uang muka sebelum bangunan selesai dan lunas begitu bangunan selesai. Jadi, produk properti Evergrande ditunggu oleh mereka dan para calon pembeli yang lain.

Modal Lehman Brothers sendiri hanya sekitar USD 25 miliar, tetapi menjelang pailit pada 2008, modal itu habis dan Lehman Brothers menderita minus modal karena ketatnya kredit perbankan dan banyaknya investor yang menarik modal mereka dari pasar uang. Rasio modal sendiri terhadap kewajibannya naik dari 24:1 selama 2003 menjadi 31:1 menjelang akhir 2007. Lehman Brothers tidak langsung memegang perumahan yang dikreditkan atau dijaminkan. Lehman Brothers hanya memegang CDO terbitan lembaga kredit perumahan dll. Ketika para debiturnya tidak mampu bayar, krisis keuangan global mulai, harga CDO jatuh tajam dan Lehman Brothers pailit.

Catatan: Lehman Brothers adalah penyebab Krisis Keuangan Global 2008. Karena itu, the Bank for International Settlements (BIS; Bank Penyelesaian Transaksi Perbankan Internasional) menaikkan rasio wajib modal inti terhadap aset tertimbang menurut risiko (ATMR, RBC) dari 4,5% menjadi 7% plus buffer (penyangga) 3,5% dan CAR total minimum 12,9% (gabungan modal Tier 1 + Tier 2) dengan modal Tier 2 minimum 2% terhadap ATMR.

Sumber: www.bis.org: A History of Minimum Risk-based Capital Requirements

4. Utang Evergrande amat kecil bagi Sektor Keuangan (Perbankan, Dana Pensiun & Perusahaan Sekuritas) China dan Dunia

Aset sektor keuangan China (perbankan, dana pensiun & perusahaan sekuritas) per akhir Juni 2021 berjumlah USD 57,56 triliun, atau USD 57.560 miliar, dan utang Evergrande kepada sektor keuangan China maupun investor LN berjumlah sekitar USD 66,6 miliar, jadi hanya 115/100.000 (0,115%) dari aset sektor keuangan China, yang tidak mencakup pasar modal (gabungan pasar saham & pasar uang). Selain itu, USD 20 miliar dari utang itu berupa obligasi yang dipegang oleh para investor LN.

5. Masalah terbesar Evergrande ada di China (domestik).

Kewajiban LN-nya yang USD 20 miliar hanya 6,6% dari jumlah kewajiban konsolidasinya yang USD 302 miliar.

6. Aset konsolidasi Evergrande yang USD 352 miliar hanya bernilai sekitar 11% dari nilai aset 100 pengembang properti terbesar China yang bernilai sekitar USD 3,3 triliun.

7. Di bawah Evergrande, ada tiga besar developer: Country Garden (aset per akhir 2020: USD 310 miliar), China Vanke (USD 248,4 miliar; BUMD Shenzhen) dan Greenland Holdings (USD 215 miliar; BUMD Shanghai), yang aset gabungannya sekitar USD 773,4 miliar per akhir 2020.

Sumber: Laporan keuangan Masing-masing per akhir 2020

8. Jumlah utang/pinjaman Evergrande (USD 66,6 miliar) teramat kecil terhadap Aset Gabungan Sektor Keuangan plus Pasar Obligasi China (USD 74,56 triliun)

Gabungan jumlah aset sektor keuangan (USD 57,56 triliun) plus nilai pasar obligasi China (USD 17 triliun) adalah USD 74,56 triliun, atau USD 74.560 miliar.

9. Kelemahan Evergrande:

9.1 Ekuitas konsolidasi hanya USD 54,7 miliar per akhir 2020, atau cuma 15,3% dari total aset USD 356,7 miliar. Untuk mengimbangi kewajiban yang besar itu, Evergrande melakukan pre-marketing, penerimaan uang muka dan cicilan sampai properti yang bersangkutan selesai dan siap huni, penjualan produk-produk pengelolaan kekayaan dsb.

9.2 Secara non-konsolidasi, ekuitas Evergrande sudah minus USD 20 miliar per akhir 2019, walaupun membaik menjadi sekitar plus USD 18 miliar per akhir 2020, atau 5,07% dari jumlah aset yang USD 313,3 miliar.

9.3 Evergrande terbiasa memberikan bunga yang tinggi (7%-20% per tahun) kepada para pembeli obligasi maupun surat berharga lainnya. Evergrande menerbitkan banyak commercial paper yang berjangka pendek (di bawah satu tahun).

10. Penolong Potensial untuk Evergrande

10.1 Banyak partner minoritas di proyek-proyek besar di China dan LN. Mereka adalah penolong terdepan dengan membeli saham-saham Evergrande di proyek-proyek kerja sama atau patungan mereka.

Contoh: Evergrande New Energy Vehicle Group (ENEH) & Evergrande Property Services Group (EPS) sebagai Perusahaan Anak yang Besar dengan Potensi Dijual Cash dan mendapatkan Miliaran USD

Pada awal Januari 2021, ENEH bernilai pasar USD 24 miliar & EPS USD 20 miliar.

11. Kesimpulan

Para mitra besar Evergrande berpotensi takeover saham Evergrande di proyek-proyek kongsi mereka. Cukup bagi Evergrande menggalang dana cash USD 25 miliar untuk meyakinkan para investor dll bahwa Evergrande akan mampu memenuhi kewajibannya.

Selain itu, para Pemda 354 kota, terutama yang makmur, misalnya Beijing, Shenzhen, Shanghai dll, di seluruh China tempat Evergrande punya ratusan proyek berpotensi membeli atau takoever proyek-proyek Evergrande di daerah masing-masing.

Contoh:

9.1 Pemda Shenzhen, lokasi kantor pusat Evergrande, punya 33,4% di China Vanke, developer nomor 3 di China yang asetnya USD 248,4 miliar per akhir 2020 dan bernilai pasar USD 35 miliar per 24 September 2021. Pemda Shenzhen, yang merupakan Pemda kota tingkat satu (Tier 1) terkaya nomor 3 di China setelah Beijing dan Shanghai, juga punya Shenzhen SASAC (Pengelola & Pengawas ratusan BUMD Shenzhen) dengan aset USD 632 miliar IDR 9,164 kuadriliun), atau sekitar 1,09 X aset gabungan BUMN se-Indonesia (IDR 8,4 kuadriliun) per akhir 2020 saja.

9.2 Pemda Provinsi Sichuan, tempat Evergrande punya banyak proyek yang bernilai miliaran USD, adalah pemilik Sichuan SASAC dengan aset USD 2,38 triliun (IDR 33,88 kuadriliun)(https://equalocean.com/briefing/20210918230080335) per akhir Juli 2021, atau sekitar 4 X aset gabungan BUMN Indonesia per akhir 2020 (IDR 8,4 kuadriliun).

A high degree of optimism about China’s economic future and better job opportunities prevails among most recent college graduate. This is good news for Chinese government and corporate leadership and foreign business players in the country.

Untuk lebih cepat menjadikan China punya GDP yang terbesar ke-2 di dunia setelah AS, negeri dengan segala macam infrastruktur umum yang termoderen, tercanggih, terbanyak, terpanjang, terluas, terbesar dan terlengkap di dunia, negeri eksportir terbesar di dunia dan penghasil produk biji-bijian yang terbesar di dunia, China membentuk tiga bank yang khusus secara sekaligus, sebagai pelaksana kebijakan (policy bank), pada tahun 1994 sehingga menjadi juara satu di seluruh dunia di bidangnya masing-masing sejak beberapa tahun lalu.

Catatan: 1. Aset CDB di tabel di atas berasal dari tahun 2018; 2. Shanghai Pudong Development Bank (SPDB) didirikan pada 28 Agustus 1992 dan adalah salah satu BUMD milik Kota Shanghai yang khusus untuk membantu membangun Kecamatan Pudong di Shanghai.

Aset itu 3,85 X kuota setoran modal 190 negeri anggota IMF (USD 687 miliar, di luar persediaan setoran kuota/modal tambahan menurut skema New Amendment to Borrowings (NAB); https://www.imf.org/en/About/Factsheets/IMF-at-a-Glance).

Aset CDB itu juga sekitar 4,1 X gabungan aset 4 lembaga anggota Kelompok Bank Dunia (USD 643 miliar: IBRD (USD 317 miliar), IDA (USD 219 miliar, IFC (105 miliar) & MIGA (USD 1,7 miliar) menurut laporan keuangan setiap lembaga itu per akhir Juni 2021 (https://www.worldbank.org/en/news/press-release/2021/08/09/world-bank-group-releases-fy21-audited-financial-statements); atau 1,9 X gabungan kuota setoran modal semua anggota IMF itu dan aset gabungan 4 lembaga anggota Kelompok Bank Dunia per akhir Juni 2021.

Buku lengkap oleh dua orang wartawan senior dan editor Bloomberg tentang sejarah & sepak terjang CDB, yang mereka juluki sebagai “Superbank China.”

Contoh-contoh proyek besar yang didanai oleh CDB:

Three Gorges Dam (Bendungan Tiga Ngarai; pembangunan selama 1994-2004): Pembangkit listrik yang terbesar di dunia dengan kapasitas 22.500 MW, jaringan irigasi dan bendungan yang juga terbesar di dunia, dengan biaya sekitar IDR 446 T

2. Bendungan & PLTA Baihetan, terbesar kedua di dunia, dengan kapasitas 16.000 MW, memakai 16 buah turbin pembangkit listrik yang masing-masing terbesar di dunia: 1.000 MW. Pembangunannya, dengan biaya IDR 484 T, sudah tuntas dan sudah memasang 4 buah turbin per akhir Juli 2021. Semua turbin itu akan selesai pada 2022.

3.Proyek Kereta Api Cepat/Peluru Jakarta-Bandung, semula IDR 60 T, sedang dibangun;

4.China-Africa Development Fund (CAD Fund; 2007), dengan modal awal sekitar IDR 150 T;

5.China-Latin American Cooperation Fund (China-LAC Fund; 2013);

6.Aneka proyek di Venezuela sekitar IDR 600 T sejak 2008;

7. Silk Road Fund (Dana Jalan Sutra; modal IDR 570 T; 2014) bersama-sama SAFE, Eximbank of China, & China Investment Corporation (CIC);

8. Dll.

Ribuan proyek pembangunan infrastruktur lain, modernisasi perkotaan dll di China telah dibiayainya.

Bank grosiran, artinya tidak menerima pembukaan rekening tabungan, deposito, rekening koran, tidak menerbitkan kartu kredit, kartu debet dan sejenisnya.

Sumber dana: 2.1 Modal: 100% dari pemerintah China; 2.2 Dana Pihak Ketiga: penjualan obligasi lewat pasar antar-bank maupun bursa efek dalam negeri plus LN.

CDB: sangat profesional dan berorientasi agak komersil karena mencari sedikit laba sambil mendorong pelaksanaan program pembangunan pemerintah China di dalam dan luar negeri. Labanya ditumpuk untuk menjaga CAR dll. Jika laba mereka tidak mengimbangi kenaikan jumlah DPK, CDB akan mendapatkan suntikan modal dari pemerintah China.

China Eximbank: 2.1 Tidak beroperasi secara komersil; 2.2 bertugas menyediakan kredit ekspor-impor kepada para pengusaha China plus para mitra maupun pelanggan LN mereka; 2.3 Tidak diwajibkan mendapatkan laba. Jadi, jika biaya operasi tertutupi oleh pendapatan operasi, itu sudah bagus bagi pemerintah China!!!; 2.4 Sukses mereka ditentukan oleh sukses pembiayaan ekspor China ke seluruh dunia. Catatan: Tugas pembiayaan ekspor juga diemban oleh hampir semua bank China yang lain.

Pemegang Saham CDB per akhir 2020

Keterangan: 1. Ministry of Finance= Kementerian Keuangan; 2. Central Huijin Invetsment Ltd, perusahaan sub-holding di bawah China Investment Corporation (CIC), perusahaan pengelola dana pemerintah (sovereign weltlh fund; SWF) yang terbesar kedua di dunia milik pemerintah pusat China dan melapor langsung ke Majelis Negara, yaitu kabinet China. Per akhir 2020, CIC punya aset total USD 1,222 triliun (USD 17,7 kuadriliun), dengan nilai aset bersih USD 1,1 miliar; 3. Buttonwood Investment Holding Co. Ltd milik SAFE (Dinas Pengelolaan Valuta Asing, yang mengurus cadangan devisa China sejumlah USD 3,2 triliun), salah satu lembaga di bawah PBoC (Bank Rakyat China; bank sentral China); 4. National Council for Social Security Fund (Majelis Nasional Pengelolaan Dana Jaminan Sosial).Gambar: logo CIC, dari websitenya

Untuk lebih cepat menjadikan China punya GDP yang terbesar ke-2 di dunia setelah AS, negeri eksportir terbesar di dunia dan penghasil produk biji-bijian yang terbesar di dunia, China mendirikan tiga buah bank [China Development Bank (CDB), China Eximbank & Agricultural Development Bank of China (ADBC)] yang bersifat khusus secara sekaligus pada 1994 untuk melaksanakan kebijakan (policy bank) pemerintah China sehingga menjadi juara satu di seluruh dunia di bidangnya masing-masing sejak beberapa tahun lalu.

Perbedaan antara Permodalan dan Dana Pihak Ketiga (DPK) Bank-Bank BUMN itu dan Ketiga Bank Pelaksana Kebijakan itu

a. Bank-bank umum yang BUMN itu plus bank-bank umum lain yang juga milik pemerintah China semula didirikan dengan modal pemerintah, mencari DPK melalui penerimaan deposito, rekening tabungan maupun rekening berjalan baik eceran maupun perusahaan (korporasi), menerbitkan obligasi dll. Banyak yang sudah go public sehingga permodalan mereka mengikuti aturan bursa efek mereka.

b. Ketiga bank pelaksana kebijakan itu: didirikan dengan 100% modal awal dari pemerintah dan belum go public.

b.1 CDB & China Eximbank adalah bank grosiran sehingga tidak menerima deposito dari masyarakat dan mencari DPK hanya melalui penerbitan obligasi dan modal tambahan dari pemerintah China. Karena itu, di China, CDB adalah penerbit obligasi yang terbesar kedua setelah Kementerian Keuangan China (https://cdn.gihub.org/umbraco/media/2617/china-case-study.pdf).

CDB punya hanya 37 kantor cabang tingkat 1 dan 4 kantor cabang tingkat 2 di Daratan China plus 1 kantor cabang di Hong Kong, ditambah 10 kantor perwakilan di LN, yang mencakup kantor perwakilan di Indonesia.

Di China, China Eximbank punya hanya 32 kantor cabang dan satu kantor perwakilan di Hong Kong. Di LN, ada kantor cabang di Paris, kantor perwakilan di St. Petersburg, kantor perwakilan untuk Afrika Bagian Selatan dan Timur plus Kantor Perwakilan untuk Afrika bagian Utara dan Barat (www.eximbank.gov.cn).

China Development Bank(CDB; Bank Pembangunan China), bank pembiayaan pembangunan yang terbesar di dunia (https://www.swfinstitute.org/fund-rankings/development-bank), yang asetnya sekitar USD 2,651 triliun (IDR 38 kuadriliun) menurut laporan tahunan 2020-nya. Aset itu sekitar 4,2 X gabungan aset perbankan umum Indonesia yang sekitar IDR 9 K.

Aset itu atau 3,88 X kuota setoran modal 190 negeri anggota IMF (USD 687 miliar, yang tidak mencakup persediaan setoran kuota/modal tambahan menurut skema New Amendment to Borrowings (NAB); https://www.imf.org/en/About/Factsheets/IMF-at-a-Glance).

Aset CDB itu juga sekitar 4,1 X gabungan aset 4 lembaga anggota Kelompok Bank Dunia (USD 643 miliar: IBRD (USD 317 miliar), IDA (USD 219 miliar, IFC (105 miliar) & MIGA (USD 1,7 miliar) menurut laporan keuangan setiap lembaga itu per akhir Juni 2021 (https://www.worldbank.org/en/news/press-release/2021/08/09/world-bank-group-releases-fy21-audited-financial-statements); atau 2 X gabungan kuota setoran modal semua anggota IMF itu dan aset gabungan 4 lembaga anggota Kelompok Bank Dunia per akhir Juni 2021.

2. China Eximbank (Bank Ekspor-Impor China), asetnya sekitar USD 781 miliar per akhir 2020 (http://english.eximbank.gov.cn/News/AnnualR/2020/), atau 1,2 X aset gabungan 4 lembaga Kelompok Bank Dunia, atau 1,13 gabungan kuota setoran modal semua anggota IMF.

Inspirasi untuk Indonesia: kita punya LPEI, yang sering disebut sebagai Indonesia Eximbank, yang asetnya berjumlah IDR 92,1 T (USD 6,35 miliar; dengan kurs USD/IDR= 14.500) per akhir 2020, turun dari IDR 108 T per akhir 2019. Aset sebanyak USD 6,35 miliar itu jelas sangat kurang untuk mendukung ekspor Indonesia dibandingkan dengan ekspornya selama tahun 2020 yang berjumlah USD 163,31 miliar (www.kemenkeu.go.id).

3. Agricultural Development Bank of China (ADBC), bank pembiayaan sektor pertanian yang terbesar di dunia, yang asetnya sekitar USD 1 triliun.

Catatan: ADBC berbeda dari Agricultural Bank of China (ABC atau Agbank; Bank Pertanian China), bank umum terbesar ke-3 di dunia dalam hal aset (USD 4,26 triliun, atau IDR 61,9 kuadriliun), yang sudah go public di Shanghai.

Sekitar 98% aset perbankan China adalah milik bank pemerintah China pada tingkat pemerintah pusat (BUMN) dan daerah (provinsi dan kota; BUMD).

A. Modal Inti 144 Bank China berjumlah IDR 42,6 Kuadriliun(K) per akhir 2020

1. Di antara 1.000 bank umum yang terbesar di dunia, yang masing-masing punya modal inti minimum IDR 7,876 triliun2 (USD 547 juta, berdasarkan kurs tukar USD/IDR= 14.400), China punya 144 dengan gabungan modal inti2 sejumlah IDR 42,6 K (https://www.thebankerdatabase.com/index.cfm/search/ranking), atau hampir 2 X jumlah modal inti milik 178 bank terbesar di AS (IDR 22,75 K), atau 4,58 X jumlah aset semua bank umum di Indonesia. Modal inti perbankan China itu naik sebesar 18,6% dari yang tercatat per akhir 2019; sebaliknya, modal T1 perbankan AS naik hanya 8,5%.

1Bentuk-bentuk modal utama yang termasuk dalam struktur modal sebuah bank adalah modal inti [core capital; Common Equity Tier 1 (CET1) capital], Modal Tier 1 dan Modal Tier 2. “Tier” berarti “tingkat.” Modal inti (CET1) berperingkat paling tinggi dan terdiri atas saham biasa, laba ditahan, agio saham yang berasal dari penerbitan saham biasa dan saham biasa yang dipegang oleh perusahaan anak milik bank yang bersangkutan [https://corporatefinanceinstitute.com/resources/knowledge/finance/common-equity-tier-1-cet1/). Modal inti juga mencakup akumulasi pendapatan keseluruhan yang lain plus cadangan lain yang diumumkan dan penyesuaian menurut peraturan perbankan dalam perhitungan CET1 (Dokumen yang berjudul: RBC20 – Calculation of minimum risk-based capital requirements, yang merupakan bagian dari dokumen yang berjudul: RBC – Risk-based capital requirements), tetapi tidak mencakup segala macam saham preferens dan kepentingan non-pengendalian.

Modal total Tier 1 (Tingkat 1) adalah gabungan CET1 dan modal Tingkat 1 tambahan (AT1; additional Tier 1). AT1 bisa terdiri atas obligasi subordinasi yang abadi (perpetual subordinated bond); contoh: BNI berencana menerbitkan sekuritas modal senilai USD 600 juta yang tergolong AT1 yang bersifat abadi dan non-kumulatif dengan kupon/suku bunga 4,3% per tahun (https://finansial.bisnis.com/read/20210917/90/1443714/perkuat-modal-bni-bbni-rilis-perpetual-bonds-rp852-triliun-kupon-43-persen). AT1 juga mencakup cadangan yang diumumkan dan saham preferens yang tidak dapat ditebus kembali dan yang bunganya juga boleh ditumpuk (non-cumulative) (www,investopedia.com).

Sekarang, bank dengan modal inti minimum IDR 7,876 triliun masuk ke KBMI 2 karena, menurut Pasal 147 POJK itu, bank digolongkan berdasarkan Kelompok Bank berdasarkan Modal Inti (KBMI): KBMI 1: modal inti <IDR 6 triliun; KBMI 2: >IDR 6 triliun sd 14 triliun; KBMI 3: >IDR 14 triliun sd 70 triliun; KBMI 4: >IDR 70 triliun.

Berdasarkan Pasal 8 POJK No.12/POJK.03/2020 (https://www.ojk.go.id/id/regulasi/Documents/Pages/Konsolidasi-Bank-Umum/pojk%2012-2020.pdf; mulai berlaku per 17 Maret 2020), per akhir 2021, setiap bank harus bermodal inti minimum IDR 2 triliun; per akhir 2022, setiap bank harus bermodal inti minimum IDR 3 triliun. Bank pembangunan daerah (BPD) diberi keistimewaan: kewajiban modal inti minimum IDR 3 triliun itu harus dipenuhi per akhir 2024.

2Berdasarkan Perjanjian Basel II, modal inti sebuah bank harus minimum 8% dari nilai aset tertimbang/menurut risiko (ATMR; risk-weighted asset). Angka itu dinaikkan menjadi 10,5% berdasarkan Perjanjian Basel III (https://www.investopedia.com/ask/answers/043015/what-difference-between-tier-1-capital-and-tier-2-capital.asp) dan rasio modal keseluruhan (capital adequacy ratio; CAR) minimum 12,9%: 10,9% merupakan modal inti minimum dan 2% merupakan modal T2. Kenaikan itu adalah salah satu tanggapan terhadap Krisis Keuangan Global tahun 2008 (https://www.bis.org/basel_framework/–Basel Committee on Banking Supervision, Market Risk Framework in Brief).

1.1 Ada 30 Buah Bank Internasional yang Penting secara Sistem Perbankan Global (G-SIBS) menurut Dewan Stabilitas Keuangan AS

[www.fsb.org, dokumen: 2020 list of global systemically important banks (G-SIBs)]

Sumber: www.fsb.org: 2020 list of global systemically important banks (G-SIBs)

2. Modal inti 144 bank terbesar China itu merupakan 30% dari jumlah modal inti (IDR 142 K) milik 1.000 bank yang terbesar di dunia. Modal inti 178 bank terbesar AS (IDR 22,75 K) merupakan15,9% dari modal inti 1.000 bank itu.

3. Secara gabungan, 144 Bank terbesar China dan 178 Bank terbesar AS kuasai 45,9% (IDR 65,35 K) dari modal inti (IDR 142 K) 1.000 bank yang terbesar di Dunia

4. Perbandingan Modal Inti 4 Bank Terbesar China & Dunia vs DBS Singapura

Catatan:

ICBC, CCB, ABC & BoC adalah empat di antara 30 buah bank yang tergolong G-SIBs.

Mayoritas saham Development Bank of Singapore (DBS), bank umum yang terbesar di ASEAN dalam hal modal inti, laba dan aset, dipegang oleh Temasek, perusahaan pengelola kekayaan pemerintah [sovereign wealth fund (SWF)] Singapura.

1. 1.Berdasarkan jumlah aset, keempat bank milik China itu juga merupakan bank-bank yang terbesar ke-1, ke-2, ke-3 dan ke-4 di dunia menurut Standar-Standar Pelaporan Keuangan Internasional (IFRS). JPMorgan Chase adalah yang ke-5 dan Bank MUFG (Jepang) ke-6.

2.Persaingan antara JPMorgan Chase dan Bank MUFG. Berdasarkan Prinsip-Prinsip Akunting yang Disetujui secara Umum di AS (US GAAP), JPMorgan Chase adalah bank terbesar ke-6 di dunia dan MUFG ke-5. Perbedaannya: IFRS menghitung nilai aset turunan secara bruto sedangkan US GAAP menghitungnya secara bersih.

B. Laba sebelum Pajak (LSP) Perbankan China mencapai 37,2% (IDR 5,01 K) dari LSP Gabungan (IDR 13,47 K) 1.000 Bank terbesar di Dunia

LSP perbankan China itu naik sebesar 5,2% dari yang tercatat per akhir 2019. Sebaliknya, LSP perbankan AS anjlok tajam sebesar 31,5%. Lihat diagram di bawah ini.

Table 1: Laba dan Peringkat Laba sebelum Pajak (LSP) Perbankan 5 Negeri

B.2 Gabungan LSP Perbankan China di atas yang Perbankan AS, Jepang, Kanada & Perancis

B.3 Perbankan China nikmati 69% (lebih dari 2/3 atau IDR 5,01 K) dari Gabungan Laba sebelum Pajak (IDR 7,26 K) Perbankan di Asia Pasifik

Peta Asia Pasifik

C. Gabungan 144 buah bank China dengan modal inti minimum IDR 7,876 memegang 25,6% (IDR 547,80 K, atau USD 38,05 triliun) dari jumlah aset 1.000 bank terbesar di dunia itu (USD 148,6 triliun).

Catatan:

CBIRC (Komisi Pengaturan Perbankan dan Asuransi China) menerbitkan laporan pada 11 Mei 2021 bahwa per akhir Maret 2021, jumlah aset 192 bank umum China, yang beroperasi di China plus cabang-cabang LN mereka, dalam Yuan (CNY; RMB) dan valas mencapai IDR 725.000 T*, atau IDR 725 kuadriliun (K; 1015), naik sebesar 9% dari yang tercatat per akhir Maret 2020 (www.cbirc.gov.cn: Supervisory Statistics of the Banking and Insurance Sectors – 2021 Q1 Statistics, diterbitkan pada 11 Mei 2021).

Nilai itu adalah sekitar 2,3 X jumlah aset perbankan AS yang sekitar IDR 315 K* (https://fred.stlouisfed.org/series/TLAACBW027SBOG: Total Assets of All Commercial banks, 08/04/2021), atau 1,4 X jumlah aset perbankan Uni Eropa (UE) yang IDR 515,77 K* (https://www.ecb.europa.eu/press/pr/date/2021/html/ecb.pr210805~0aea16eb0a.en.html: ECB publishes consolidated banking data for end-March 2021), atau sekitar 78 X jumlah aset perbankan umum Indonesia yang IDR 9,3 K per akhir Maret 2021(Laporan Profil Industri Perbankan-Triwulan 1 2021 oleh OJK).

*Sampai saat ini, mirip perbankan Uni Eropa (UE), perbankan China masih dominan dalam penyediaan dana ke sector ekonomi China karena pasar obligasi China masih sedang tumbuh (baru bernilai pasar sekitar IDR 288 K). Sebaliknya, aset perbankan AS lebih kecil daripada aset pasar obligasi AS (IDR 662 K) yang terbesar di dunia. Perbedaan lainnya: (i) Baru sekitar 2,9% dari nilai pasar obligasi China dimiliki oleh investor asing; (ii) sekitar 30% dari nilai pasar obligasi AS maupun UE sudah dimiliki oleh investor asing.

C.1 Perbandingan Aset Perbankan China vs UE & AS per akhir Maret 2021

Perbankan China adalah pendorong terbesar pertumbuhan ekonomi, teknologi, militer, infrastruktur dll di China. Sekitar 60% aset mereka adalah tabungan rakyat dan perusahaan swasta China.

China, an example of a nation developing its economy through high savings rates.

No developing country is known to get rich from the consumption sector of their economy. Most rich countries have got their wealth from their manufacturing activities, called as the secondary sector, with different levels of technological complexity, now or in the past. The percentage contributions of the primary and secondary sectors to their GDP have been declining in the past 50 years. For example, what the UK and the US have seen in their GDP compositions.

It is true that they began developing their countries with the primary sector, including agriculture. Then, they shifted most of their economic activities to the secondary sector, and saved most of their disposable income, accumulating wealth. Once they reached the level of adequate affluence, they started consuming more of their income, and hence, lowering the ratios of both their savings as well as investment to GDP. As a result, their saving rates have been relatively very low. See the chart below.

In addition, developing countries with a high (>60%) ratio of public and household debts to their GDP, coupled with a similar ratio of their external loans to GDP and a low ratio of savings to GDP, have found themselves struggling to pay interest charges and/or repay debts. Their economies are also vulnerable to both internal and external financial and other shocks.

Reasons: Investment has a reproductive effect, but consumption does not. Consumption supports life and health and occasionally helps maintain an unsustainable standard of living to a certain extent. As a result, the higher a country’s ratio of consumption expenditure to its GDP, the less money its households and businesses save and the less money they both have for investment. As a further result, its GDP growth rate declines and its consumption ratio to GDP goes up. In order to prevent further declines, its households and government must borrow money heavily and/or the latter monetizes its debts.

Many countries with similar situations have even borrowed much more to survive the current Covid-19 pandemic. For example, the UK, Japan and the US.

In addition, consumptive nations tend to demand a higher and standard of living. In the long run, their consumption can exceed income, and they will begin to live beyond their means and have to borrow money to keep their standards of living. The most recent example is what the US has been experiencing in the past 50 years: change of international standing from a creditor to debtor nation (https://www.latimes.com/archives/la-xpm-1985-09-17-mn-20088-story.html).

Unsustainable Consumption (combined with corruption) can get a country bankrupt

CAVEAT: Certain individuals and businesses have got so wealthy from the consumption sector. For example, Hartono brothers of the famous Djarum group, ranked first in terms of wealth in Indonesia; Zhong Shanshan, the king of water and the wealthiest person in China and Asia.